Four perspectives on Telco enterprise business growth in 2023

Four perspectives on Telco enterprise business growth in 2023

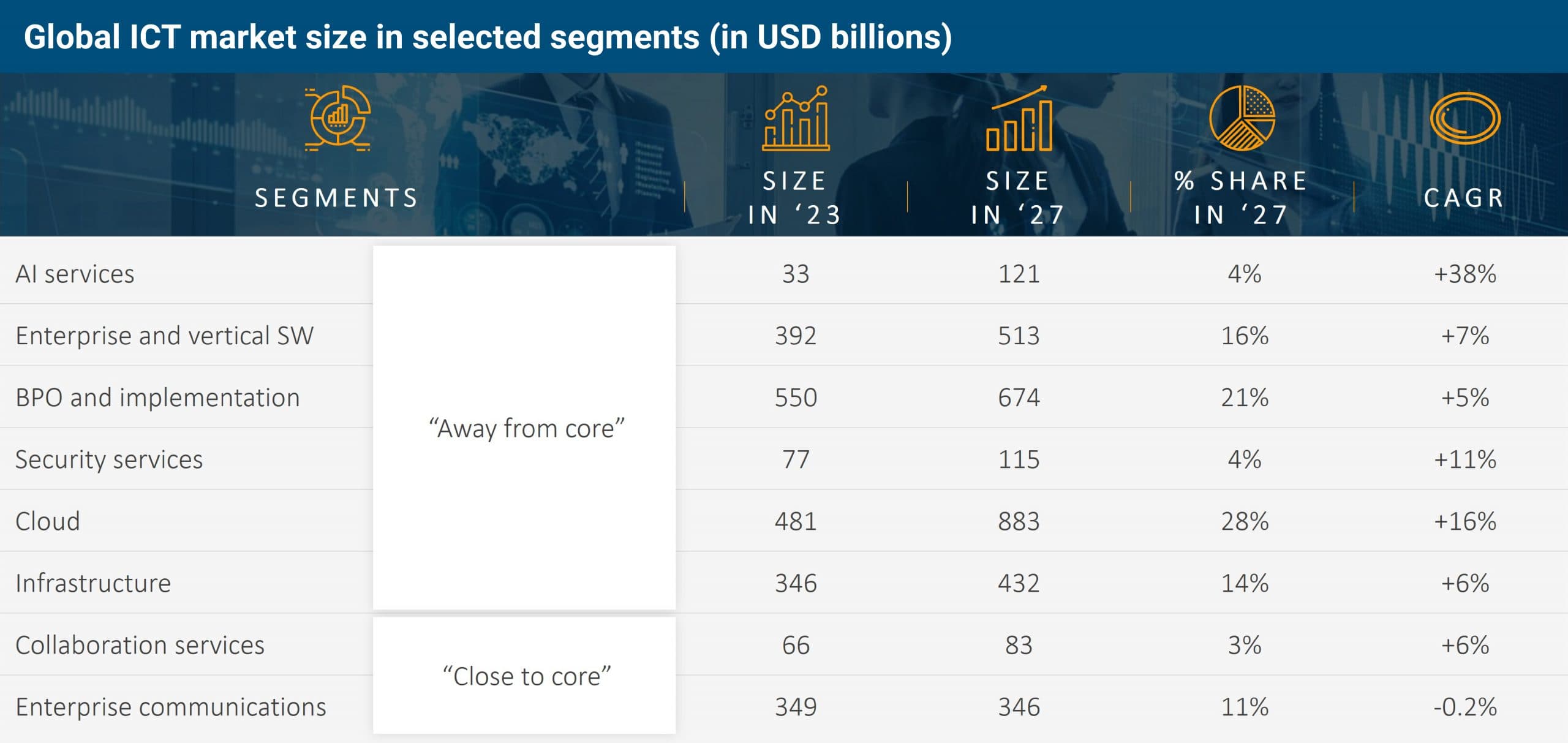

The market for enterprise information and communications technology (ICT) is expanding rapidly, with particular hot spots in the domains beyond traditional network services.

The year 2023 is expected to bring continued expansion to this market despite economic uncertainty and cost pressures. To reap their fair share of the opportunity, telcos must focus on building internal ICT business readiness and capability.

We emphasize four perspectives on the enterprise telco growth opportunities for 2023, including mastering solution-selling, balancing core business management and new ICT revenue streams, and exploring hotspots in cybersecurity and cloud services.

Enterprises’ ICT spending continues to grow globally with a shift in spending patterns

The global ICT demand will grow at a projected >10 percent CAGR in the coming years despite the brief slowdown during the pandemic. Enterprises, both large and small, are expected to increase their ICT spending although the change in the spending patterns is already discernible.

The pandemic-induced mass transition to hybrid working and “forced adoption” of digitalization have far-reaching implications on how enterprises plan their ICT strategies and spending for the years to come. One significant change is the ongoing industrialization and capability expansion for seamless and secure hybrid working models. Similarly, enterprises are investing more in accelerating the transition to resilient and highly automated operations.

Many expect that the enterprise workforce will permanently adopt hybrid ways of working in more than 60-80 percent of companies worldwide. This is a clear shift to an increasingly distributed organizational model that requires new types of tools and practices to function at scale. The existing enterprises investments in digitalization and public cloud migration are foundational in this shift.

Accordingly, we believe that the migration of IT to the cloud continues as enterprises globally still have significant room to move workloads to the cloud, There is likely to be an increasing amount of scrutiny over the specific workloads to be moved and how best to re-architect systems for the cloud environment. For companies — 40-60 percent of all enterprises that have undergone a cloud transformation— a priority will be to optimize the new cloud-enabled operations and manage the ROI of cloud investments made. On the other hand, a hybrid multi-cloud strategy will be in the crosshairs for the majority of large enterprises as most seek to reduce the negative impacts of deep single-vendor lock-in.

Illustration #1. Key shifts in enterprise ICT spending patterns and key hot spots

Telcos need to be on the ball with client demands and increase their ICT maturity relentlessly

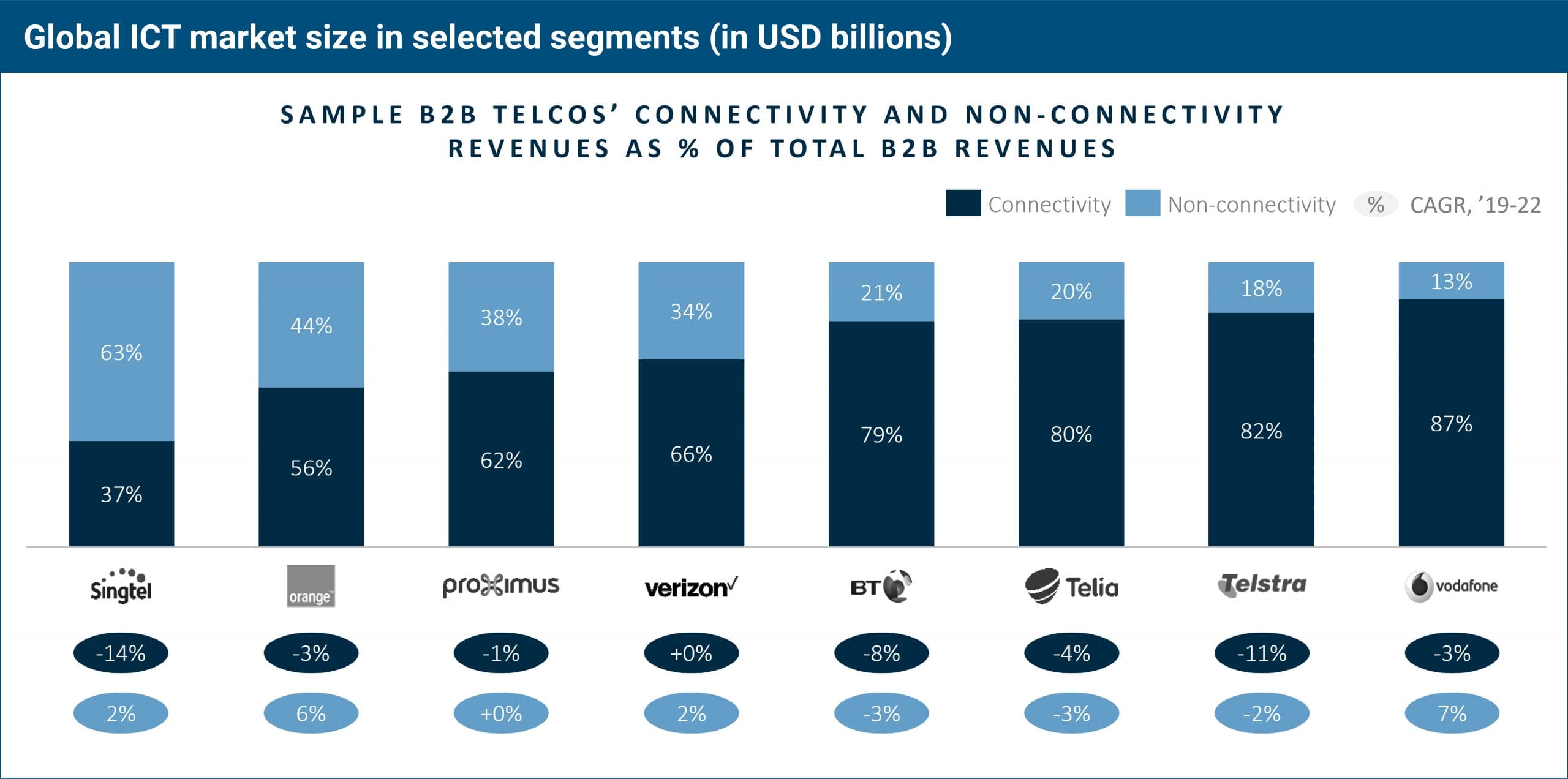

In the past, even the leading telcos with a dedicated IT arm have experienced modest success beyond core network-services. The share of B2B revenues for a typical telco is around 10 percent, and a specialized B2B-focused Telco can reach over 25 percent of total revenues. Across the board, the composition of Telco B2B revenues today is still connectivity-services dominated.

Leading players such as Singtel, Telstra, Orange and AT&T can generate over 15-30 percent of their enterprise revenues through non-connectivity ICT services. These services include offerings such as managed IT and outsourcing services, cyber security, cloud, systems integration services etc.

Regardless of current B2B business maturity, there is a strong consensus that the enterprise segment and IT solutions and services will be a major growth opportunity for telco around the world and highly synergistic with the extensive 5G infrastructure investments being deployed. The key question that remains is “What will it take for telco to thrive in B2B beyond the core?”

Success in Enterprises’ business necessitates several things from telco. Leveraging the core network investments to deliver innovative connectivity services is an obvious action. On top of that, Telcos will need to navigate increasingly competitive B2B markets and build new enablers for Enterprises business growth. In our experience, B2B buyers expect five key conditions from their preferred strategic ICT providers and transformation-partners:

Deep solution expertise that goes beyond the technical domains

Deep industry understanding and thought leadership

Solutions that are at the same time innovative, reliable and secure

Ability to provide turn-key and managed-services solutions

Ability to orchestrate other vendors and partners so as to reduce implementation risk

Illustration #2. Telco enterprises revenue composition + cagr examples summary

To win the battle for customer ownership and to sustain and grow enterprise share of wallet (and mind), telcos’ industry and ICT specialization have to increase. Leading ICT-specialized telcos must possess high maturity across several critical areas — ICT offerings, go-to-market strategies and supporting capabilities; and they are advanced as well in their ability to generate pull-through sales for the core telco offerings through solutions and a professional services-led account-expansion approach.

Economic uncertainty, inflationary macro-environment and geopolitical tensions are creating an unpredictable backdrop for 2023. Despite the unpredictability and risk of utter economic and geopolitical turmoil, telcos need to push forward to advance their B2B and ICT agendas. Keeping a laser focus on market developments and changing customer needs is imperative.

For this article, we have chosen four distinct perspectives on how telcos can drive enterprise business growth in 2023. Although this list is by no means exhaustive, we believe that it reflects some of the priorities that telco management teams and enterprise business leaders should have on the agenda.

Illustration #3. Four perspectives on driving enterprise business growth in 2023

Improving the ICT business-readiness through enabling sales

Selling ICT is different from selling traditional network services-oriented products in many ways. ICT products are more complex and typically involve many vendors and interrelated technologies; the sales cycles are longer and involve a variety of functional stakeholders (and motives); and accordingly, ICT products are sold as integrated solutions that necessitate a consultative selling approach.

We believe that 2023 should be the year when telco enterprises double down on modernizing their B2B selling capabilities and enable an industry-savvy ICT salesforce. Building strong relationships and preferences as a partner requires interaction with people, processes, and technology capabilities. The gains for the leaders appear in the form of deeper client engagement and improvement in deal hit-rates and margins.

A world-class sales enablement engine connects marketing and sales efforts through real-time insights, governance, people, and technological capabilities. The three major pillars of empowerment are (1) analytics-led selling, (2) digital sales-knowledge management, and (3) end-to-end digitalization of the lead-to-quote process.

The business value derived from analytics-led selling and digital knowledge-management capabilities relates to several factors. Leaders can produce rich analytical insights to guide all aspects of the deal-pursuit decision-making. Such insights include understanding the value potential of each opportunity, being able to predict win-rates, applying the right pricing tactics and profiling of buyers to fine-tune the selling approach. Deep analytical insights should inform every step of the deal-management process. For example, predictive analytics can be utilized modularly to build personalized sales presentations based on content that is scored as most engaging or impactful. Similarly, specialized tools enable tracking of client- and prospect-engagement with shared sales materials and proposals (e.g., time spent on specific pages, sharing forward, etc.).

Furthermore, the more digitalized and analytics-led the sales process is, the clearer the visibility provided to the sales leadership. Key information on deal velocity, deal margins, probabilities, and sales-team activities will help manage the sales efforts and teams based on facts.

Leading telcos organize the whole lead-to-quote process for maximum sales effectiveness and impact. This means aligning the teams and practices to cater to the high-stakes strategic client-and deal-pursuits, infusing sufficient industry- and solution-expertise where required, and integrating decision-making across the sales, pricing, legal, finance and partner stakeholders of the deal team. Digitalization and automation have a lot to offer to the building of a seamless collaboration backbone for the bid-management process.

The next evolution in the enterprise sales-enablement tool landscape will be driven by fast-moving players adopting generative AI-based functionalities for deeper personalization of sales engagement and sales collateral creation. This will significantly increase the time a sales team will be able to spend where it matters, i.e., together with the client understanding their needs and the suitable solutions.

Supporting enterprise transition to digital and hybrid work

Remote working models were adopted rapidly at the beginning of the pandemic era, and today hybrid work has become the mainstream model for over 70 percent of enterprises.6 Many enterprises onboarded new remote-working tools and practices in a relatively unorganized manner resulting in diverse approaches across units and functions. Going forward, macroeconomic uncertainty and rising prices are likely to lead to a simplification of the unified communications- and collaboration-landscape in many enterprises.

Despite the apparent need for rationalization, enterprise adoption of solutions for enabling hybrid work is set on a steady growth trajectory. The market for unified collaboration and communications was $43bn in 2022 and is expected to be $46bn in 2023. This implies an increase of 7 percent for the year. Cloud-based collaboration is a specific hot spot in the UCC space. Microsoft Teams has to date accomplished amassing a monthly active-user base of nearly 280 million, up from only 20m in 2019. This figure comprises both private users as well as more than one million enterprise customer-users. Microsoft Teams have become a highly dominant platform, gradually displacing the competition. In a market where Enterprises is likely to employ only one or two collaboration services, the competition is going to intensify.

Telco is recognized as a key channel for enterprises to source their communication and collaboration platforms and services. The possibility to bundle UCC offerings with network services and broader value-added services and technical support is highly appealing to any enterprise that appreciates simplicity and convenience.

Furthermore, Telco can play a key role in helping large enterprises and SMBs rationalize their portfolio of collaboration tools, migrate legacy solutions to the cloud and provide necessary support and managed services. Managed services specifically are highly regarded by SMBs as the only feasible model for small companies without extensive in-house technical expertise and IT personnel.

2023 will be a year of economic uncertainties as well as growth in enterprise communications and collaboration spending — and an area in which Telco needs to build and maintain strong capabilities to serve the needs of their enterprise clientele. Leaders globally have done just that, for example:

Telstra Purple in Australia set up a dedicated Microsoft practice and a 5-year strategic agreement with Microsoft jointly to drive enterprise hybrid work and cloud transformation in Australia (February 2023)

Singtel in Singapore enhanced its UCaaS/CPaaS software with Zoom’s solutions for fixed-line integration and immersive meetings — it has seen a 25 percent year-on-year increase in UC adoption in its base since the launch in 2021 (January 2023)

Several Telco outlets in North America and € ope (BT, Telia, Verizon, Swisscom, and Rogers) have become partners for Microsoft Teams Operator Connect Mobile with enterprise-grade secure mobile calling with Teams (late 2022).

Becoming the trusted advisors for enterprises’ cloud transformations

The enterprise shift to the public cloud and associated growth in cloud-spend is projected to grow at a CAGR of >20 percent for the years 2021-25. By 2025, the enterprise cloud-spend should exceed the traditional IT spend in application, system and infrastructure software, and business-process-services segments (41 percent of total IT spending in 2022, growing to 51 percent in 2025).

Today we can see two clear segments of enterprises when it comes to the cloud. The first segment comprises the enterprises that have just started their journeys or are still in the early stages of cloud adoption. These companies seek to capitalize on the initial cost-saving effect and architectural flexibility that public-cloud migration promises. The current challenging economic outlook combined with rising energy prices keeps enterprises driving the execution of their cloud strategies in 2023 with high certainty.

The second segment comprises enterprises that have invested in their cloud transformations over the past several years and are now increasingly focused on maximizing the ROI from these efforts. This group of enterprises wants to keep the consumption costs in check with high predictability and rectify any mistakes in the planning and execution of the initial waves of cloud migration. Furthermore, a significant portion (70-80 percent) of large enterprises are gravitating toward a hybrid multi-cloud strategy that combines several cloud providers and public and private cloud infrastructures. For many, this can mean rethinking the initial cloud migration decisions and, more broadly, is driven by a need to reduce vendor lock-in and to get the most business value out of the cloud investments (e.g., resilience, innovation, business performance, etc.).

Cloud transformation is a significant and growing opportunity for telcos globally. Leading telcos grow their professional and managed services offerings in this space and continue to focus on hybrid multi-cloud enablement for their large enterprise clients. However, telcos must think about what role they want to play in the full value realization of enterprise digital and cloud transformations.

We expect enterprises to flesh out the artificial intelligence strategies and investment plans in numbers over the coming years. Thus, what used to be siloed, small IT-led technology projects will become larger bodies of coordinated transformation initiatives.

Unsurprisingly, the perfect alliance between data and artificial intelligence will become the sought-after endgame for the cloud transformations that are now in motion. Digitalization and cloud adoption increase the volume and velocity of enterprise data and the centralization of that data. These, on the other hand, are the key enablers for the “next wave in digitalization” — enterprise AI adoption at scale.

2023 should be the year when telcos strive to become the cloud advisors and thought leaders for their enterprise customers, for both the business and IT stakeholders. The emphasis needs to be on continued enterprise-cloud-enablement but also increasingly on supporting the enterprise customers to chart the next stages in the cloud journey and on building offerings to help extract more business value across the organization.

The leading Korean telco player, SK Telecom, has already announced an AI strategy and vision that underpin its path to becoming an “AI Company”.

The announced strategy has several internal and external initiatives. For example:

Adoption of AI use cases in its core operations

Driving hyper-personalized front-end customer experience

Facilitating the enterprise customers’ AI transformations via its six business areas (data centers, private networks, IoT, cloud, big data and AI)Monetization of the fast-growing AI HW segment through a dedicated AI semi-conductor venture

Innovation of new AI-enabled servicesThe cloud domain is going to evolve fast, and it will be critical for telcos to see the implications on possible new services and offerings that go beyond realizing IT-centric cost savings and optimizing the enterprise cloud spend.

Meeting the digital enterprises needs for a robust cybersecurity posture

The expected developments in the cybersecurity space are, to a great extent, tied to enterprise digitalization and cloud migration and to the transition toward hybrid work models whereby the work is increasingly conducted outside the enterprise premises. As a result, the exposed surface for various types of cyber threats is going to increase. The estimate of the total economic loss caused by cybercrime varies between USD 1-7 trillion annually and is growing faster than the enterprise cybersecurity-spend (15 percent versus 8-12 percent annually).

Global evidence on telcos’ success in cybersecurity is limited although many are actively pursuing growth in the space.. This has often occurred through a partnership-led approach but in some cases with direct investment into building their cybersecurity ventures. These undertakings did well during the pandemic and are expected to do so going forward. For example:

Ensign (a JV between StarHub and Temasek): Revenues in 2019 were S$146mn and S$301mn in 2022, and CAGR in 2019-22 was 27 percent. Regional Asia Pacific expansion is the key future-growth driver for Ensign.

Orange Cyberdefense: Revenues in 2019 were €580mn and €977mn in 2022. CAGR in 2019-22 was 19 percent. Orange has built its cyber business through partnerships and acquisitions and has had the carve-out of OCD in its plans for a while.

Telco enterprise cybersecurity offerings vary in breadth and depth. Similarly, the needs of large enterprises with operations in several countries are different from an SMB with a national presence. Absent in-house IT and cybersecurity expertise, smaller enterprises are reliant on service providers for packaged, modular, and managed services-enabled security solutions.

The need for more stringent cloud-based security measures and secure authentication to enable new virtual and remote-work models has catapulted the growth of Secure Access Service Edge (“SASE”) solutions. SASE solutions integrate and package what is essential for hybrid-work models; SD-WAN and cloud security components delivered in an SaaS model. The global SASE market is expected to surpass $9 billion in 2023. That means a growth of 40 percent compared to the market size in 2022.13 Growth will be fastest in the SMB segment, where there is a high preference for a single-vendor turnkey-solution.

By 2025, over 60 percent of enterprises are likely to have adopted SASE or at least to have an implementation strategy in place.14 In our view, telcos are in the pole position to drive the adoption across large and SMB enterprises. Through connectivity-bundled solutions and by providing standard and premium features to accommodate the business scale differences, telcos can build attractive value-propositions for their customers. The big promise of SASE can be in its synergies with 5G network slicing, in enabling end-to-end security across the whole 5G ecosystem across public cloud, private cloud, edge and the enterprise.

Conclusion

The global enterprise ICT market opportunity is sizeable and growing. However, it is fastest-growing in domains outside of traditional network services. Economic uncertainty and cost pressures persist in 2023, and although most enterprises will thoroughly scrutinize their ICT spending, the market overall will continue to expand. The shift in spending is expected to continue as enterprises push to digitalize across operations, offerings, customer experience and workforce.

Our four perspectives on enterprise telco growth opportunities for 2023 emphasize the importance of building internal ICT business readiness and capability. Successful players will master the complexities of solution-selling and find a balance between managing core business and nurturing new ICT revenue streams. Telcos need to pursue growth close to the core and at the same time explore the enterprise ICT hot spots — such as cybersecurity and cloud services.

FTI Delta telco-, B2B-, and ICT-business experts work with leading enterprise telcos globally. We help our clients address the fast-changing competitive landscapes and solve the most complex business challenges — guiding from strategy to execution. Our unique industry-specialist capabilities and global network of experts enable us to help in devising strategies that are execution-ready and to surface the “True North” for your enterprise growth journey.

Please reach out to our FTI Delta experts to start a conversation.